GUEST POST: Private Credit: Expanding Beyond Senior Secured Lending

Overview:

- Private credit continues to grow as institutional and individual investors seek alternative sources of income and diversification beyond public fixed income markets.

- While senior secured lending has traditionally been a cornerstone of private credit, asset-backed finance (ABF) has gained traction as a complementary strategy offering collateral-backed protections.

- Floating-rate structures in both senior secured loans and ABF help mitigate interest rate risk in rising rate environments, reducing interest rate sensitivity compared to traditional fixed-income instruments.

- While both benefit from floating-rate structures, corporate cash flow lending and asset-backed finance take different approaches, offering complementary roles in private credit with varying risk profiles, return drivers, and liquidity considerations.

- Investors evaluating private credit should consider a balanced allocation across senior secured and ABF strategies to optimize income generation, enhance downside protection, and improve overall portfolio resilience.

Broadening the Private Credit Landscape

Advisors are increasingly exploring private credit to enhance client portfolios, recognizing it as a distinct alternative investment alongside other semi-liquid vehicles, such as non-traded REITs. Like these investments, private credit is best suited for long-term allocations due to its illiquid nature. While non-traded REITs have introduced many investors to private markets, private credit offers another entry point with distinct opportunities. This paper explores the evolving private credit landscape, the factors driving its growth, and the role of asset-backed finance (ABF) as a key component.

What’s Driving Private Credit’s Growth?

Once a niche market, private credit has become mainstream due to several converging factors:

- Regulatory-Driven Bank Pullback – Stricter post-GFC regulations and the 2023 regional banking crisis have forced banks to reduce lending, limiting financing options for middle-market businesses and institutional borrowers. From 2000 to 2020, the number of U.S. commercial banks declined from over 8,300 to 4,227, creating a gap that private lenders have filled.[1]

- Shifts in Interest Rate Policy – Floating-rate debt structures in private credit adjust with rate movements, reducing interest rate risk compared to traditional fixed-income investments.

- Compelling Yield Differentials – Private credit has consistently offered higher income potential with better risk-adjusted returns than most public fixed-income alternatives, often in the 9-12%[2] range, making it an attractive option for investors seeking enhanced return profiles.

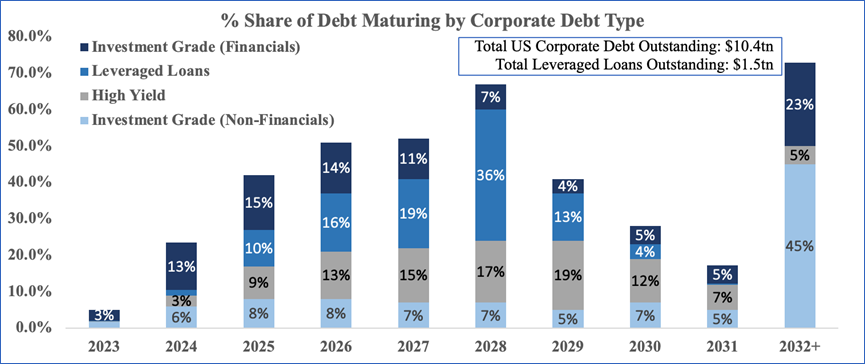

- Rising Refinancing Demand – With an impending “maturity wall” of corporate debt set to come due in the next few years, non-bank lenders are expected to play an increasing role in refinancing and restructuring transactions (see chart below).

Source: Goldman Sachs, The Impact of Rising Rates on Corporate Debt & US Equities, October 30, 2023.

Senior Secured Lending: A Foundation of Private Credit

While private credit encompasses a variety of lending strategies, senior secured direct lending has traditionally been a cornerstone of the space. It has become the primary alternative for middle-market and sponsor-backed companies seeking financing solutions outside traditional banks. While several factors contribute to this growth, two key drivers are:

- Acquisition & Growth Financing – Private equity firms rely on senior secured loans to finance buyouts and strategic expansions, as banks have become less willing to underwrite leveraged transactions.

- Floating-Rate Advantage – Floating-rate structures help mitigate the impact of rising rates, making these loans more adaptable to shifting economic conditions than conventional bonds.

Private Asset-Backed Finance (ABF): Expanding the Private Credit Playbook

Beyond corporate credit, private asset-backed finance (ABF) has expanded into a significant segment of private credit, offering distinct benefits. By 2007 – before the Global Financial Crisis – specialized funds were structuring long-duration, asset-backed investments outside traditional hedge fund strategies. One such vintage-year structured asset-backed fund, which I helped underwrite, was designed to house select transactions from an asset-backed hedge fund, featuring a longer duration and more intricate structuring than the hedge fund’s typical portfolio. While not unprecedented in hedge fund structures, it was relatively novel to private equity investors, reflecting the early stages of ABF’s evolution into a distinct private credit strategy.

Since then, ABF has evolved beyond its early structures, including CDOs, expanding into a specialized private credit strategy that continues to leverage tangible or financial assets as collateral – now across a wider set of financing applications and market participants. Some of the primary advantages include:

- Enhanced Downside Protection – Loans are backed by assets, reducing credit risk through collateralization and structural safeguards.

- Expanding Investment Universe – New financing structures have emerged across industries, particularly in:

- Infrastructure financing (e.g., data centers and renewable energy projects)

- Transportation and equipment leasing

- Consumer finance (e.g., installment loans and trade receivables)

- Intellectual property and royalty-backed transactions

- Trade Finance (specialized short-term credit facilities supporting global trade)

- Structural Safeguards – Many ABF investments incorporate:

- Collateral reserves to create protective buffers for investors

- Tiered repayment structures that prioritize senior claims on cash flow

- Amortization structures that gradually reduce outstanding principal

- Ongoing asset valuation assessments to monitor risk exposure

- Market Dislocations Driving Growth – Disruptions in public structured credit markets have opened opportunities in sectors like consumer and aviation finance. As traditional capital sources retreat, private ABF lenders are increasingly filling these gaps, driving broader adoption of structured private credit solutions.

Comparing Private & Public Credit Structures

| Characteristic | Private ABF | Public ABS | Private Senior Secured Loans | Public Leveraged Loans |

| Primary Repayment Source | Cash flows from tangible or contractual assets | Aggregated cash flows from diversified loan pools | Business revenues and enterprise value | Corporate cash flows |

| Risk Mitigation Approach | Asset collateralization & highly-structured security | Rating-based credit enhancement | First-lien seniority with covenants | Covenant-lite structures increasing risk exposure |

| Liquidity Profile | Limited secondary market, customized transactions | Highly liquid, with active securitization markets | Moderate liquidity with some secondary trading | High liquidity in syndicated loan markets |

| Market Adoption & Growth | Growing in specialty finance & niche credit markets | Well-established, mature securitization market | Growing as banks reduce lending activity | Deep market with broad institutional participation |

Strategic Considerations for Investors

A well-structured private credit allocation can enhance stability, improve returns, and hedge against volatility. While senior secured lending provides direct exposure to corporate cash flow lending, asset-backed finance offers collateral-backed protections that reduce reliance on a borrower’s enterprise value alone. In constructing a diversified private credit allocation, investors should consider combining both approaches to optimize income generation and risk management:

- For Capital Preservation & Stability – Senior secured lending offers floating-rate exposure and downside protection through first-lien positions.

- For Yield Enhancement – Asset-backed finance provides strong income generation with diversified cash flow sources, broadening the portfolio’s exposure beyond corporate lending while often incorporating floating-rate structures for interest rate protection.

Conclusion

Private credit continues to evolve, with senior secured lending and asset-backed finance serving as distinct yet complementary pillars. While senior secured loans remain essential for financing corporate acquisitions and growth, private ABF has become a key structural solution for investors seeking diversified collateral-backed exposure. As non-bank lending expands, a well-balanced allocation across both strategies can improve stability, yield, and diversification in a shifting market environment.

[1] Matt Hanauer, Brent Lytle, Chris Summers, and Stephanie Ziadeh, Community Banks’ Ongoing Role in the U.S. Economy, Economic Review, Second Quarter 2021 (Federal Reserve Bank of Kansas City).

[2] AllianceBernstein, Demystifying Private Credit Investing, September 2024. The study found private credit generated an average annualized return of 9.5% from 2004-2023.